A better solo 401(k)

Introducing a modern, all-digital solo 401(k) designed to help you deliver exceptional value to your self-employed clients.

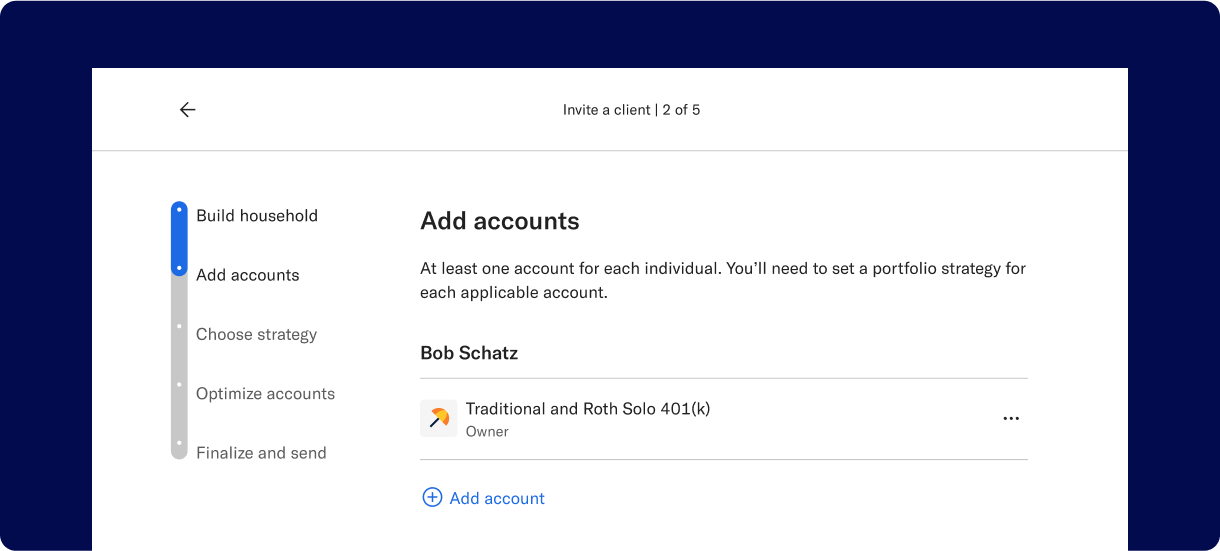

Skip the hassle with fully digital account creation, including e-signature on plan adoption agreements. Your clients can set up or convert an existing plan quickly, with zero fees for plan establishment.

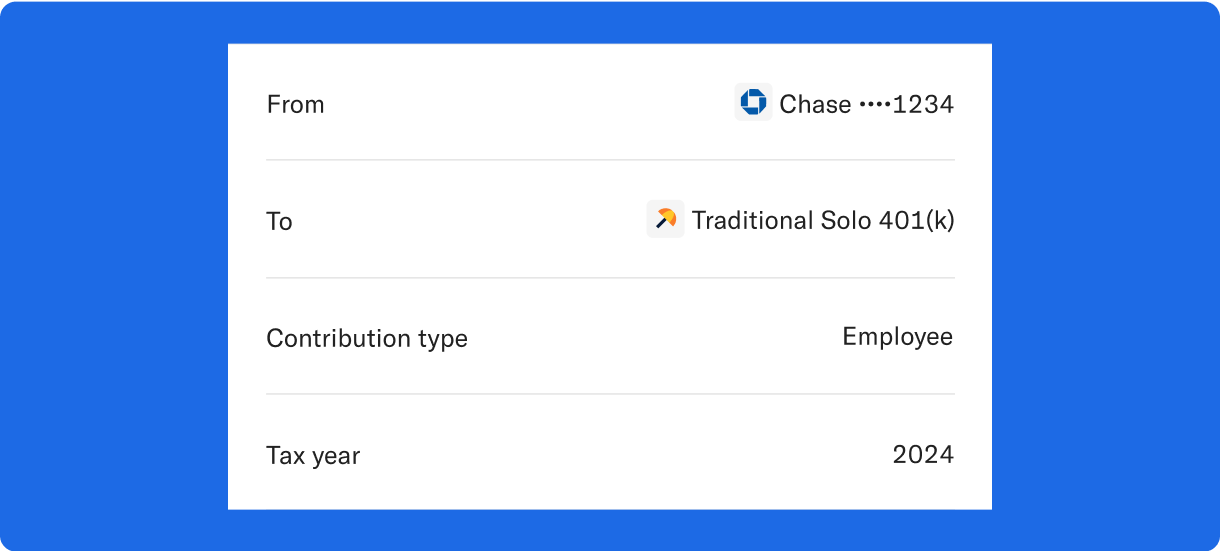

Fund in-platform—no more mailing in checks. We accommodate ACH and internal transfers for employee and employer contributions. Plus: Contributions are automatically tracked to simplify tax season.

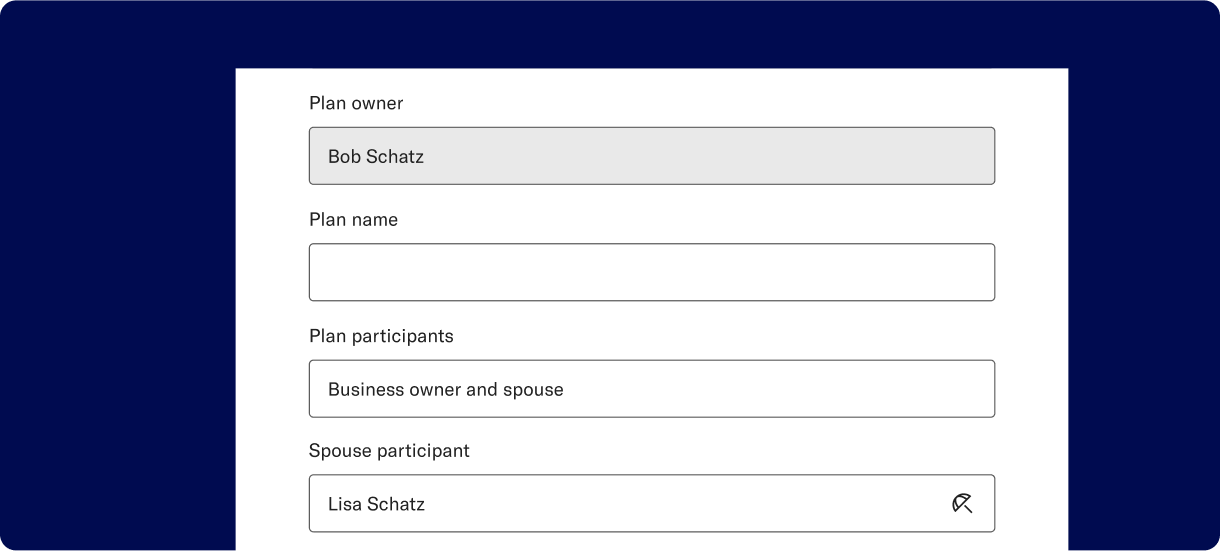

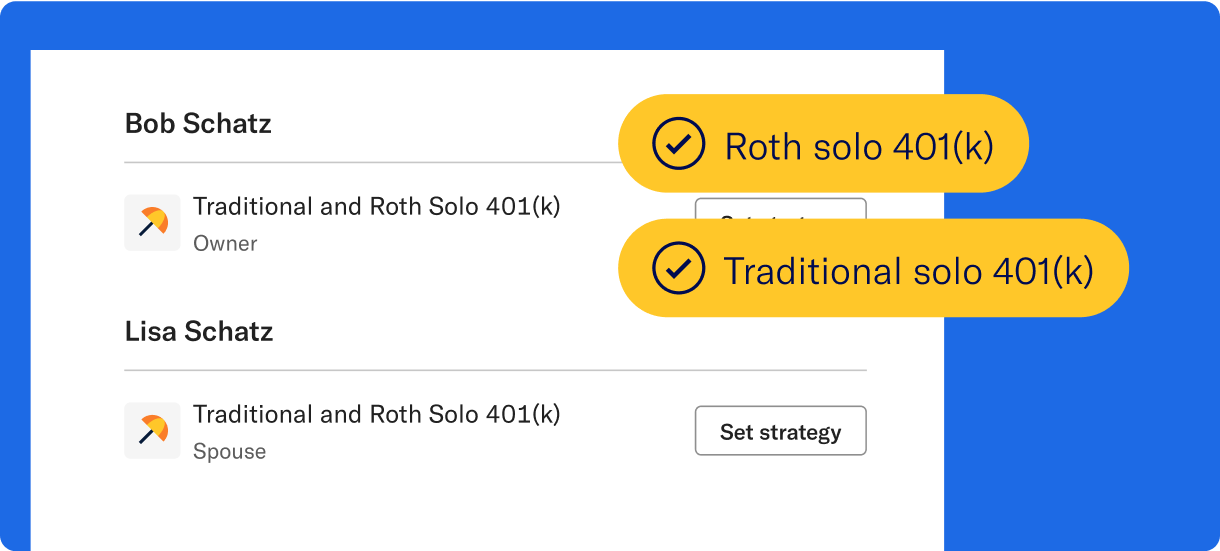

Clients can double their contributions, and their household’s retirement savings potential, by including a spouse at no extra cost.

Offer both Roth and traditional contribution options, giving your clients the flexibility to choose tax-free growth or immediate tax savings—whichever approach is best for their retirement.

Webinar: Unlock the power of solo 401(k)s

Solo 401(k)s can be a game-changer for advisors and self-employed clients. Tune in to our webinar to see how Betterment’s solo 401(k) can help you maximize clients’ tax-advantaged retirement savings and elevate your advisory services.

Retirement solutions for all.

Betterment is a comprehensive platform for wealth and retirement planning, helping you create more value for every client. Manage IRAs and taxable investing accounts for individuals and families, alongside solo and group 401(k) plans for business owners and employers, all in one platform.