Invest in an IRA.

Earn up to $1,000.

Open an IRA (or any individual investing account) and complete a qualifying deposit or rollover to get some extra money on us. Terms apply. Click below to enroll in this promotion.

Tax benefits.

We coordinate your retirement accounts for maximum tax efficiency, helping you save on taxes and grow your returns.

Automated technology.

We make investing easy by putting it on autopilot, handling all the trading, rebalancing, and dividend reinvesting.

Retirement planning.

We build you a personalized plan, recommend how much to save, and adjust as needed.

-

900,000+

Customers

-

$50+ Billion

Assets under management

-

14+ years

In business

-

Traditional IRA

Get your tax break up front and pay no taxes until you withdraw. -

Roth IRA

Money goes in already taxed so growth and withdrawals are tax-free.

-

SEP IRA

A traditional IRA for self-employed people and small-business owners.

Have an old 401(k) or IRA? We can help roll them over easily.

Moving your retirement accounts into a Betterment IRA allows you to manage your money in one place and can save you on high fees. If you’re looking to roll over at least $20k, you can talk with an advisor about it for free.

Learn about our expert built portfolios

Our portfolios are the easy way to invest like a pro. Choose from our selection to help you build wealth over the long term.

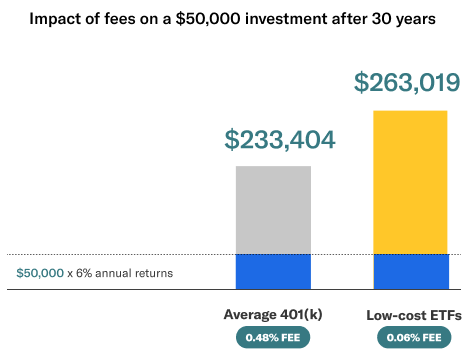

Lower fees today can mean more money tomorrow.

A 401(k) with even a modest fee may cost you tens of thousands of dollars over time. The savings from rolling into a managed Betterment IRA of low-cost exchange-traded funds (ETFs) can add up to a more comfortable retirement.

Get personalized advice on your retirement.

We offer hands-on guidance from our team of experts to help bring clarity and confidence to your retirement.

0.65% annual fee. Minimum balance required.

IRAs come with questions. We’re here with answers.

Boost your retirement with an IRA.